GG & BB turn 19 today and as I have been doing for the past few years, I thought I will write them a letter this year too. Since they will graduate next year, I thought this year’s letter will be about how they can be financially savvy and learn about money.

Dear GG & BB,

As you start to look and plan your future, money will be a huge part of how you plan your lives. Money and the lack of money may be the difference between surviving and living the life of your dreams. So you must learn to manage your finances, and manage them well enough that you never have a day when you panic about not having enough.

If you think that financial planning is too tedious and can be put off to a later date, you’re not alone. Many of your friends and peer are too caught up with life to think about long-term finances. Plus, there’s always the misconception that you can only start growing your wealth after you earned your first pot of gold. However, contrary to what you might think, the best time to start planning for your financial goals is while you’re still young and have plenty of time to grow your savings.

Set goals early: Setting your financial goals is the first critical step. Putting down your goals in writing will help you establish a finish line to aim for and determine what you need to do to get there. To help to stick to your goals, keep them somewhere you can see them regularly and also review them at a pre-determined interval, so you can fine-tune your plans as life happens.

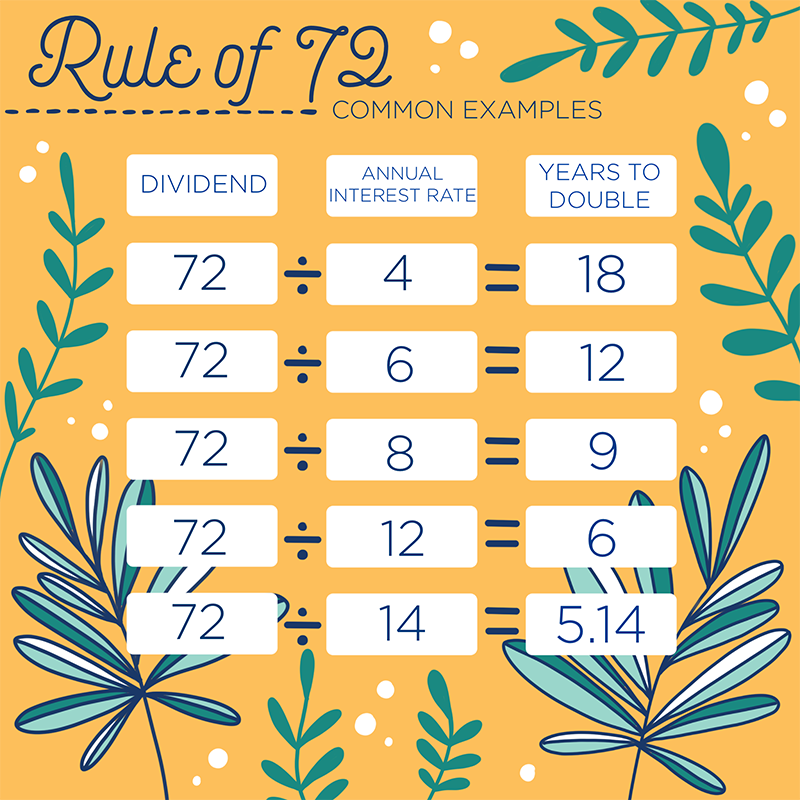

Start saving as soon as possible: Starting to save at an early age gives you a longer runway to reach your financial goals and gives you more time to benefit from the power of compound interest. There is a formula known as the Power of 72 which allows you to determine how many years it takes for your savings to double at a certain rate of interest. In the Power of 72, you divide 72 by the interest rate to determine how many years it will take to double your principal amount.

Use the 50/30/20 rule when budgeting: A simple rule of thumb is to split income into three broad buckets to meet expenses and savings needs. In this rule, divide your monthly take-home pay into three categories where 50% will be spent on needs, 30% will be spent on wants and the balance 20% will be set aside as savings.

Set up a dedicated bank account for your savings: To ensure that you don’t spend money meant for your long-term savings, it’s a good idea to open separate accounts; one for your regular expenses and another just for savings. Arrange for the funds meant for your savings to be automatically transferred to the dedicated account the day you receive your salary. You can do this by applying for a standing instruction with your bank, saving you the trouble of having to make the transfer yourself each month.

Look for ways to cut costs: Financial stability is not just about savings or increasing your income, but also about reducing expenses. Always be on the lookout for ways to save money; whether it’s finding the cheapest place to buy groceries or taking advantage of dining deals on your credit card.

Focus on income, not savings: While keeping a lid on expenses is important to budgeting, some experts recommend that you should focus more on income. After all, there are only so many of your costs that you can save on, but your income has a far higher potential to grow in the long run. If you think you are good at something, try to have a side hustle so you can supplement your income.

Keep your debt in check: Having too much debt is a big obstacle to building your savings. For a start, you should ensure that you make at least the minimum payment on all your outstanding debts every month to avoid late fees and extra interest charges. You must also always pay off your credit card bills every month. Using a credit card is a great tool, but not when you incur interest in it. A good rule of thumb is that each time you use the card, you should immediately transfer the money to the account with which you pay the bills so once the bill comes, you are not in shock. You should also list your debts from the highest to the lowest interest rate and repay as much as you can on the debt that incurs the highest interest. Keep doing this till you are debt free!

Protect your personal information: Keep identity thieves from stealing your information. Use strong passwords and change them regularly. Avoid using public wi-fi for online banking and protect your bank PIN and shield the keypad from view when using an ATM. Review your financial statements each month to make sure there are no fraudulent transactions.

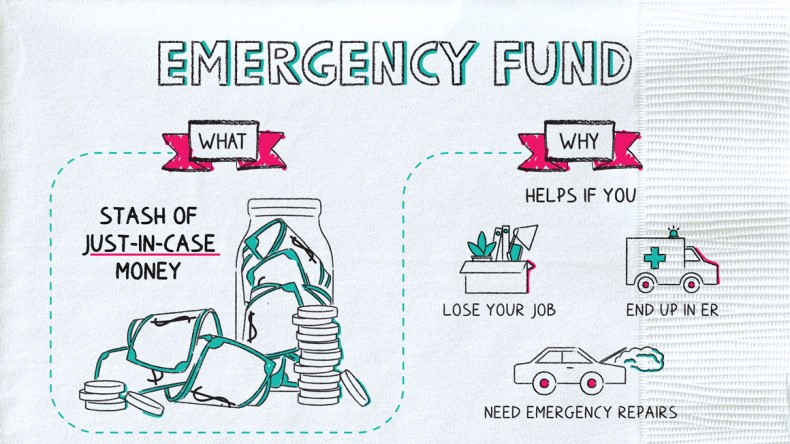

Always have emergency funds which are easily accessible: You must have at least two types of emergency funds which can be easily accessed in case of emergencies. The first should be a liquid savings account which should have about three to six months of living expenses. This is if something happens like losing your job, you can use it to get by until you are on your feet again. The second is what I call a Home Fund and this will especially be useful once you both have your homes. Try to put in a couple of hundred dollars into this account each month and maybe more when you have them. At home, things break down or you spoil and you may need to replace them. Things like a television, air conditioners etc and having money in an account meant for these things can help a long way in replacing broken items immediately without dipping into your savings.

Educate Yourself: If you don’t learn to manage your money, then other people will find ways to mismanage it for you. Some of these people could have bad intentions, others may be well-meaning, but not fully informed about your circumstances, so the best way to get the right advice for your particular circumstances and not rely on random advice is to take charge of your financial future and read a few basic books on personal finance. Once you’re armed with knowledge, you know what works best for you.

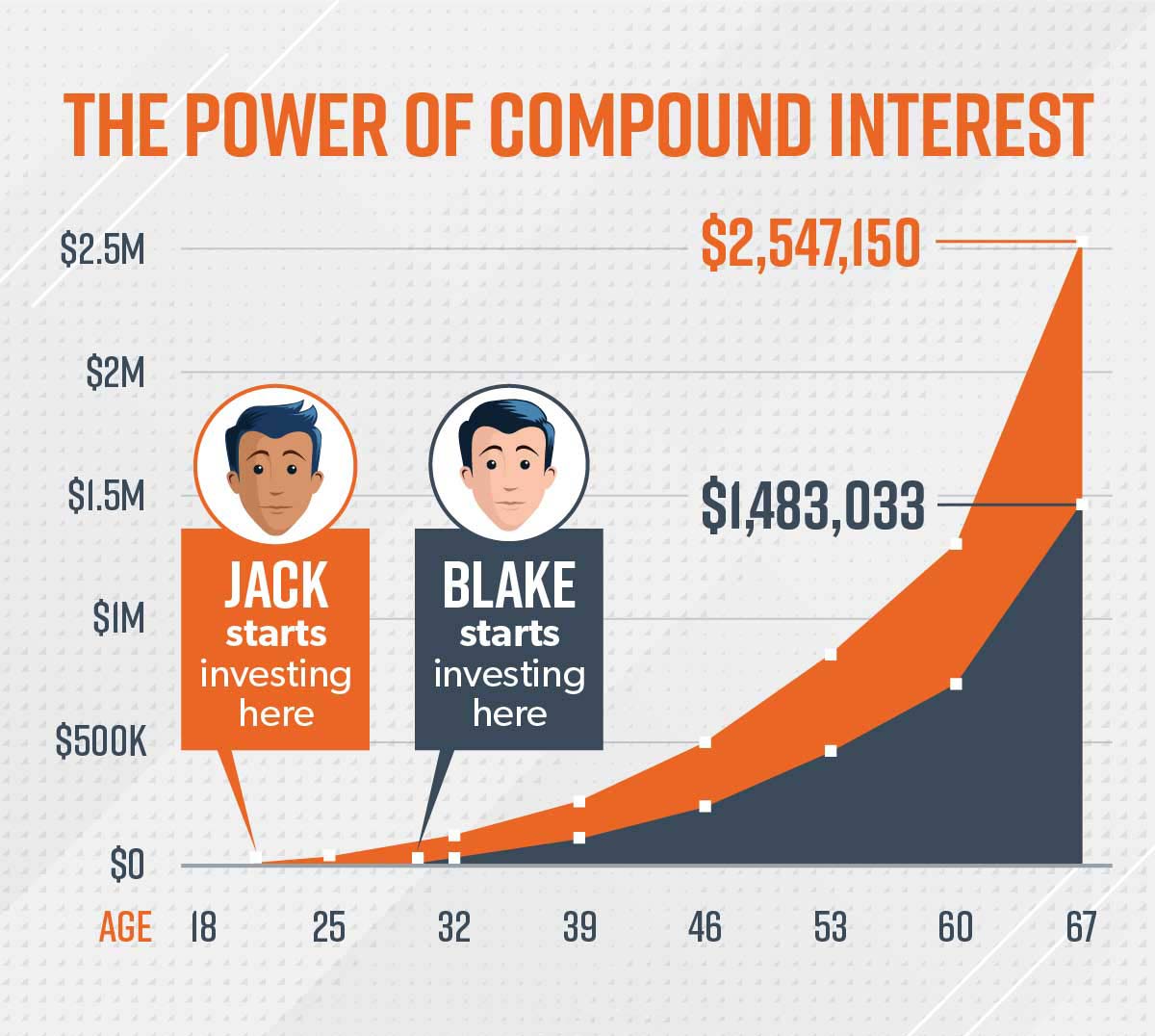

Start saving for retirement now: You may think retirement is at least four or five decades away, but you need to plan for it from today. I’ve spoken about the power of compound interest to you both, and this is the best way you can grow your money at a faster rate. The sooner you start saving, the less principal you have to invest to end up with the amount that you need to retire. Compound interest is one of the most powerful forces in finance because it grows your money exponentially, which means it can super-charge your savings, especially over time. The magic of compound interest for your retirement account is that it is interest on interest—literally. You earn interest not only on the principal which is the money you put in but also on the interest which is the money the bank pays you for holding your principal.

Remember, your finances are in your hands and you don’t need any fancy degrees or special backgrounds to become an expert at managing your finances. So go ahead and learn what you can while you are still young, so your later adulthood and retirement are not fraught with worry.

Happy birthday once again GG & BB! I know you will do great things in life and I am waiting to see you both reach your full potential.

Lots of love, hugs and kisses,

Mum

{kind=link}