As GG & BB turn 21 later this year (where did all the time go?), I decided to start a new series aimed at young adults. This series will have articles on what adulting is all about. So what is adulting? Adulting is simply doing things that an adult does – work, make and save money, buy or rent a home, etc. Today’s topic, the first in the series, will talk about a very important, perhaps the most important, aspect of adulting – financial literacy.

Being financially literate means having the knowledge and skills to make informed decisions about managing money effectively. This critical life skill empowers one to achieve their financial goals, build wealth, and secure their future.

What is financial literacy? Financial literacy encompasses understanding concepts like budgeting, saving, investing, credit, debt management, and risk protection through insurance. It involves being able to read and analyse financial statements, calculate interest rates, and comprehend the time value of money. Ultimately, financial literacy equips one with the ability to make sound financial choices that align with their short-term and long-term objectives.

Developing financial literacy early in one’s career is crucial for several reasons. Understanding credit, interest rates, and the consequences of overspending can help one steer clear of accumulating unmanageable debt, which can hinder their financial progress. Unexpected expenses like medical bills or job loss can derail finances. Financial literacy teaches the importance of setting aside funds for emergencies and providing a safety net. Whether it’s buying a home, funding retirement, or achieving other financial milestones, financial literacy empowers an individual to make informed decisions about saving and investing for their future goals. Lastly, being financially literate means understanding the role of insurance in protecting assets and income from potential risks, such as accidents, illness, or natural disasters.

One of the fundamental principles of financial literacy is the importance of saving. Developing the habit of saving early can have a profound impact on long-term financial well-being. Here are some reasons why saving should be a priority:

- Emergency fund: as mentioned earlier, an emergency fund can provide a financial cushion during unexpected events, preventing one from going into debt or depleting their long-term savings.

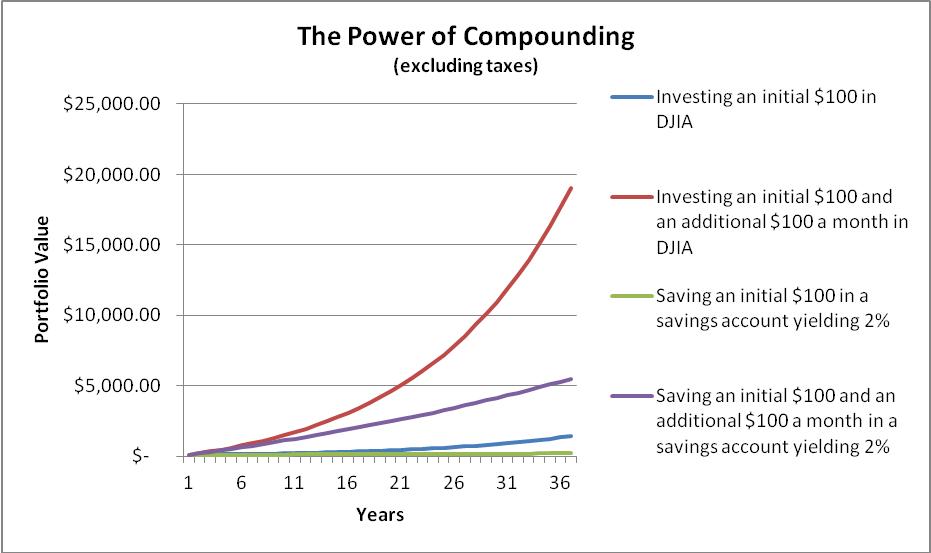

- Retirement planning: compound interest is a powerful force that can help retirement savings grow exponentially over time. Starting to save for retirement early, even with small amounts, can make a significant difference in future financial security.

- Achieving financial goals: Whether it’s buying a house, starting a business, or taking a dream vacation, saving consistently can help one achieve their financial goals more quickly.

Here are some tips for starting on a financial literacy journey:

- Create a budget to track income and expenses to understand where the money is going. Budgeting is the foundation of effective money management.

- Build an emergency fund and aim to save at least three to six months’ worth of living expenses for unexpected emergencies.

- Educate oneself by reading books, attending workshops, or taking online courses to improve one’s financial knowledge. Understanding concepts like compound interest, credit scores, and investment strategies can empower one to make better financial decisions.

- Automate savings by setting up automatic transfers from salary and other commonly used accounts to a dedicated savings account, making saving a habit and reducing the temptation to spend.

- Seeking professional advice by working with a financial advisor, especially for more complex financial matters like retirement planning or investment strategies. One should look for fee-only advisors who act as fiduciaries, putting one’s interests first.

- Once an emergency fund has been established and high-interest debts have been paid off, one should consider investing in diversified portfolios like mutual funds or exchange-traded funds (ETFs) to build long-term wealth.

The key things to focus on in building emergency funds are setting realistic goals, making saving automatic and consistent, cutting expenses where possible, and taking advantage of opportunities to direct extra money towards the emergency fund. Building the habit and making it a priority from a young age will pay off tremendously. To build an emergency fund, here are some effective ways to start:

- Start small and set achievable goals: Begin by saving the first $1,000 (or an equivalent amount in your currency) as an initial emergency fund target. Set small, realistic goals like saving $20-$100 per month until that first $1,000 is reached. Having an achievable initial goal will help one stay motivated and build the habit of saving.

- Set up automatic transfers: Automate savings by setting up recurring transfers from the main account to a dedicated high-yield savings account for the emergency fund. Treat these automatic transfers like a recurring bill that gets paid first before other expenses. Automating the process makes it easier to save consistently without having to think about it.

- Cut back on unnecessary expenses: Identify and reduce discretionary spending on things like eating out, entertainment, subscriptions, etc. Cook at home, find free/low-cost hobbies, and cancel unused memberships. Redirect the money saved from cutting expenses into the emergency fund.

- Use windfalls and pay raises: When one receives tax refunds, bonuses, gifted money or pay raises, allocate a portion towards the emergency fund. Don’t treat windfalls as extra spending money; instead, prioritise saving some of it.

Developing financial literacy is an ongoing journey, but the sooner you start, the better prepared you’ll be to navigate the financial challenges and opportunities that lie ahead. Embrace financial education, cultivate healthy money habits, and take control of your financial future from the very beginning of your career.